The zipper is one of the most underrated mechanical engineering achievements in history

@amypretzel, on X

The modern zipper was not the spontaneous invention of a single corporate entity but the result of iterative mechanical engineering in the United States over several decades. The conceptual foundation was laid in 1851, when Elias Howe Jr., the renowned inventor of the sewing machine, secured a patent for an “Automatic, Continuous Clothing Closure”. Despite this early breakthrough, Howe abandoned the pursuit, likely distracted by the overwhelming commercial success of his sewing machine.

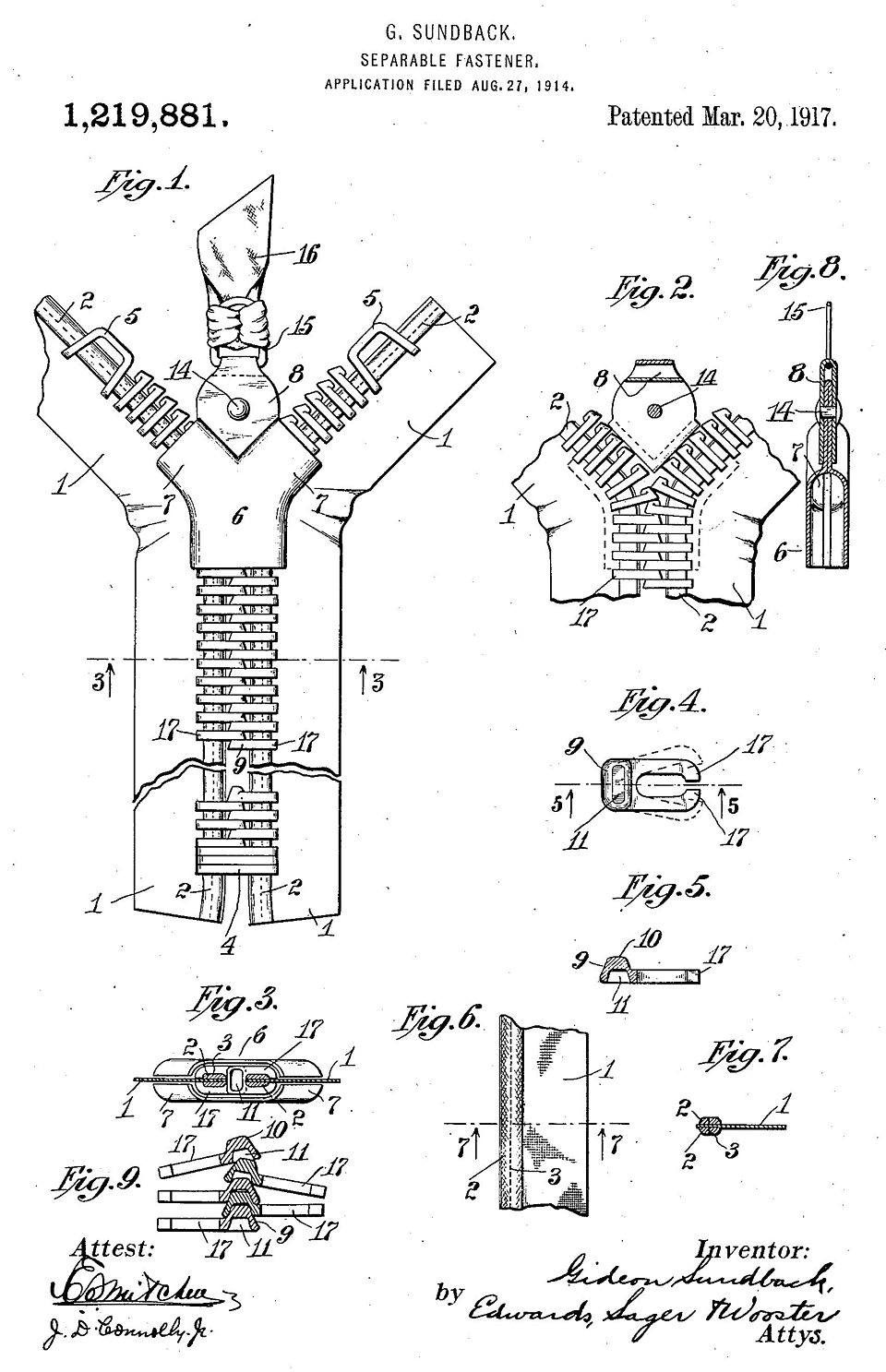

The first functional precursor to the modern zipper was developed between 1891 and 1893 by Whitcomb L. Judson. Judson debuted his "Clasp Locker" at the 1893 Chicago World's Fair, marketing it as a faster, more efficient alternative to the tedious process of buttoning boots. However, Judson’s invention was plagued by mechanical unreliability, frequently pulling itself apart under stress. It was not until the tenure of Gideon Sundbäck, the head designer at the Universal Fastener Company (which would later evolve into Talon), that the interlocking teeth design was perfected between 1911 and 1923, leading to the birth of the modern, reliable "zipper".

For the first half of the twentieth century, the American manufacturer Talon dominated the global market, capitalizing on Sundbäck's innovations. At its peak in the 1960s, Talon held an iron grip on the industry; the company's name was stamped on 70% of all zippers manufactured worldwide.

However, possessing a near-monopoly bred profound corporate complacency. Talon failed to reinvest aggressively in productivity enhancements, allowing its cost basis to swell. Furthermore, the company neglected to innovate for emerging applications. This strategic inertia left a massive vulnerability in the global market.

The void would be systematically filled by an ascendant Japanese enterprise.

The Ascent of YKK and the Doctrine of Total Vertical Integration

In 1934, a 31-year-old entrepreneur named Tadao Yoshida founded Yoshida Kogyo Kabushikikaisha, now globally recognized by its acronym, YKK. Operating initially out of Tokyo, Yoshida began by reverse-engineering Talon's designs. However, after his production facilities were decimated by firebombing during World War II, Yoshida relocated to his hometown of Kurobe to rebuild the company from the ground up, implementing a revolutionary operational philosophy that would ultimately redefine the global supply chain. Yoshida dubbed it the “Cycle of Goodness”.

Dissatisfied with the prevailing zipper production methods of the era and the prohibitive costs of imported European and American machinery, Yoshida directed his engineering teams to design YKK's own proprietary manufacturing equipment.

This directive established a paradigm of total vertical integration that remains largely unparalleled in modern manufacturing. YKK controlled, and continues to control, every conceivable stage of the zipper production process. The company smelts its own brass, synthesizes its own plastic and polyester compounds, weaves and dyes its own fabric tape, casts the interlocking teeth, and even manufactures the cardboard boxes in which the final products are shipped.

This obsessive vertical integration provided YKK with an insurmountable competitive advantage. It allowed the company to guarantee uniform, exacting quality on a truly global scale. Whether a zipper was manufactured in a YKK facility in Japan, the United States, New Zealand, or Vietnam, the components were identical, reliable, and perfectly interchangeable. By the time NASA astronauts Neil Armstrong and Buzz Aldrin walked on the moon in 1969 wearing pressurized spacesuits secured by heavy-duty YKK brass zippers, the Japanese firm had decisively overtaken Talon in both technological supremacy and market share.

YKK expanded aggressively across the globe, establishing a massive footprint that currently spans 73 countries with roughly 100 wholly-owned subsidiaries. By leveraging its vertical integration, YKK captured approximately 40% to 50% of the global zipper market by value. Today, the company produces over ten billion zippers a year, which represents more than 3 million kilometers in length or about 80 trips around the world.

The European Legacy Players: Coats and Prym

While YKK achieved unquestioned dominance in the core zip fastener market, the broader “hard haberdashery” and fastener sector1 was historically populated by deeply entrenched European legacy firms.

The most notable of these heritage entities was the German conglomerate William Prym GmbH & Co. KG. Prym’s industrial roots trace back to 1530 when Wilhelm Prym, a goldsmith, established a metal manufacturing operation in Aachen. Over hundreds of years, Prym evolved from a regional brass manufacturer into a formidable, internationally active holding company producing a wide array of textile closing systems, material technologies, and high-tech mechatronics.

Coats Holdings Ltd was the other major structural pillar of the European market. Founded in the United Kingdom, Coats originally built its reputation as a leading global manufacturer and supplier of industrial sewing and embroidery threads. Coats aggressively expanded its footprint in the fastener sector through strategic acquisitions. Most notably, in 1988, Coats acquired the major German zip manufacturer Opti. This acquisition instantly elevated Coats to the position of the world's second-largest supplier of zip fasteners, directly trailing only the YKK group.

By the latter half of the twentieth century, the global fastener and hard haberdashery industry had crystallized into a highly concentrated, impenetrable oligopoly. YKK held the premier global position in continuous zip fasteners, while legacy firms like Coats and Prym wielded immense institutional power and distribution leverage, particularly across the European continent.

This intense concentration of market power among a handful of rational, profit-maximizing corporate actors, combined with the highly specific, inelastic economic characteristics of the products they manufactured, created an ideal, low-friction environment for systemic collusive behavior.

The Microeconomics of Fastener Pricing and Inelastic Demand

In the apparel manufacturing sector, “garment costing” is a highly structured, analytical process utilized to calculate the total expenditure required to produce an item and bring it to market. This process dictates retail pricing strategies, informs sourcing choices, and directly determines the brand's overall profitability. Costing accountants typically combine all expenses into two broad categories: direct costs, which include raw materials (fabric, trims) and direct labor (cutting, sewing, finishing); and indirect costs, which encompass factory overhead, logistics, shipping, duties, and administrative expenses.

Depending on the garment's complexity and end-use, the fabric consumption can account for 40% to 70% of the total manufacturing cost. Furthermore, labor costs - often calculated through CM (Cut and Make) charges - represent another massive expenditure, heavily influenced by regional minimum wages and the technical proficiency required to stitch the garment.

Conversely, trims, hardware, and packaging - such as zippers, custom branded buttons, elastics, labels, and polybags - constitute a negligible, almost mathematically invisible fraction of the overall production cost. A high-quality, standard 14-inch YKK invisible nylon zipper (the type commonly utilized in dresses and lightweight apparel) might cost an apparel manufacturer approximately $0.32 wholesale. Even heavy-duty, separating metal zippers utilized in premium outerwear or denim jeans generally range from $1.50 to $4.00.

For an apparel brand designing a mid-tier garment, the absolute cost of the zipper is entirely immaterial to the financial viability and margin structure of the product. However, while the cost of the zipper is microscopic, the cost of a zipper failure is catastrophic. A broken, jammed, or popped zipper instantly renders the entire garment unwearable. In the retail ecosystem, this translates directly into immediate consumer returns, permanent brand damage, negative online reviews, and severe financial chargebacks from major retail distributors. So everyone exhibits extreme risk aversion regarding fasteners.

This dynamic creates severe price inelasticity of demand for premium fasteners: because the cost of the zipper is such a tiny component of the total cost of goods sold, buyers are highly insensitive to modest, incremental price increases from trusted, proven suppliers like YKK, Coats, or Prym.

In highly competitive, fragmented markets, this inelasticity naturally rewards the most reliable manufacturer with strong pricing power and healthy margins. However, in an oligopolistic market where the primary competitors secretly communicate and coordinate their pricing strategies, this inelasticity transforms from a natural market phenomenon into an easily exploitable vulnerability. The cartel members implicitly understood that if they coordinated simultaneous price increases across the entire industry, they would meet with virtually zero resistance from the buyer side of the market. There was nowhere for the garment manufacturers to turn, and the cost of the raw component was too small to justify the massive capital expenditure required for a new entrant to replicate YKK's vertical integration or Prym's historical distribution networks.

The illicit manipulation of the global fastener market was not a singular, monolithic event, but rather a multi-decade, highly sophisticated enterprise comprising several overlapping, targeted conspiracies.

Four Cartels

Following a sweeping, multi-year investigation, the European Commission formally identified four distinct cartels operating between 1977 and 2003. Each cartel was meticulously tailored to specific product categories, geographic domains, and competitive dynamics.

Cartel 1: The VBT “Work Circles” (1991–2001)

The most expansive and highly institutionalized of the conspiracies governed the massive market for “other fasteners” and their corresponding attaching machines. Running continuously from at least May 1991 to March 2001, this cartel included an extensive roster of major players: YKK, the Prym group, the American firm Scovill Fasteners, the French manufacturer A. Raymond, and the German firm Berning & Söhne.

The coordination mechanism for this cartel was deeply embedded within the industry's social fabric, operating under the guise of legitimate corporate gatherings organized by a German trade association known as the Fachverband Verbindungs- und Befestigungstechnik (VBT). The cartel operated through a series of clandestine, structured meetings famously designated in the European Commission's findings as the "Work Circles."

The primary function of the Work Circles was to agree upon and implement coordinated price increases through scheduled, annual "price rounds" (referred to internally as Preisrunde). For example, meeting minutes recovered by antitrust investigators revealed granular agreements to implement 3% to 3.5% price hikes across key target markets such as Germany, the United Kingdom, and Belgium, explicitly scheduled to take effect on specific dates in early 1993. In 1992, competitors even discussed how the corporate takeover of the Italian company Fiocchi by Prym would need to be strategically factored into future price increases.

Furthermore, the participants engaged in extensive, multi-year efforts to formulate a harmonized “European price list”. Executives explicitly discussed standardizing market prices across borders, eliminating competitive variances in Italy and Austria, and establishing unified, rigid discount rate policies to prevent sales teams from secretly undercutting the agreed-upon minimums to win large accounts.

Cartel 2: The Prym-YKK Bilateral Agreement (1999–2003)

As the broader market for "other fasteners" continued to consolidate toward the end of the 1990s, the unwieldy, multi-party circle meetings evolved into a much tighter, highly targeted bilateral conspiracy between Prym and YKK group.

Operating efficiently from 1999 to 2003, this secondary cartel abandoned the need for broad group consensus, focusing instead on direct, bilateral coordination between the two dominant players. Prym and YKK executives engaged in fixing minimum, average, and target prices on a highly granular, product-by-product and country-by-country basis.

Cartel 3: The Tripartite Zip Fastener Cartel (1998–1999)

While the first two cartels focused heavily on the intricate market for snaps, rivets, and attaching machinery, the third cartel targeted the crown jewel and highest-volume segment of the industry: the continuous zip fastener itself. From April 1998 through November 1999, the three undisputed global leaders in zipper manufacturing, YKK, Coats, and Prym, entered into a highly focused, tripartite arrangement.

The primary achievement of this tripartite group was the mutual agreement upon a distinct methodology for establishing absolute minimum prices for standard zip fasteners across the entirety of the European market.

Cartel 4: The 21-Year Non-Aggression Pact (1977–1998)

Perhaps the most astonishing of the four conspiracies, primarily due to its longevity, was a bilateral market-sharing agreement between Coats and Prym that lasted an incredible 21 years (from January 15, 1977 until, at least, July 15, 1998).

This specific cartel functioned as a classic corporate non-aggression pact. To avoid a costly war of attrition, Coats agreed to refrain from utilizing its resources to enter the “other fasteners” market. In exchange, the two entities effectively partitioned the broader haberdashery market between themselves.

The European Commission noted that this longstanding market sharing arrangement directly resulted in the automatic diversion of trade patterns from the course they would have naturally followed in a free and open market.

The Unraveling: Dawn Raids and the Economics of Leniency

Acting on preliminary, confidential intelligence, the European Commission executed a series of unannounced, simultaneous inspections (commonly referred to as “dawn raids”) at the premises of several major fastener manufacturers and the offices of the VBT trade association on November 7 and 8, 2001.

The execution of the dawn raids immediately and violently altered the risk calculus for every executive and corporation involved in the cartel, triggering a high-stakes, real-world application of the classic Prisoner’s Dilemma. Under the European Commission’s 1996 and 2002 Leniency Notices (similar to the Corporate Leniency Program utilized by the U.S. Department of Justice), antitrust regulators offer an asymmetrical incentive specifically designed to destabilize cartels.

The mechanics of leniency programs are simple but devastatingly effective: the first conspirator to break ranks, disclose the full extent of the secret cartel, and provide decisive, “smoking gun” evidence receives a massive reward: 100% immunity from all regulatory fines and, depending on the jurisdiction, protection from criminal prosecution for its executives. However, this immunity is a zero-sum game. Subsequent confessors who rush to the authorities after the first applicant are merely offered significantly reduced discounts on their eventual penalties (e.g., 20% to 50% off), scaled based on the timing of their confession and the added value of the evidence they provide.

Recognizing the sheer volume of overwhelming evidence seized during the dawn raids, absolute panic set in among the conspirators. The trust that had sustained the cartels for decades evaporated overnight, replaced by a desperate race to the regulator's door. The Prym group was the first to recognize the inevitability of the situation. By November 26, 2001 - eighteen days after the dawn raids - Prym officially applied for leniency, blowing the whistle on its long-time co-conspirators.

As a direct reward for being the first to break ranks and provide evidence of significant added value, Prym was granted full, 100% immunity from fines regarding the massive worldwide cartel for “other fasteners” and attaching machines. They also received substantial, multi-million-euro fine reductions for its verified involvement in the other related cartels.

Realizing they had been preempted by Prym and were now exposed to the full, unmitigated wrath of European antitrust law, Coats and YKK subsequently scrambled to submit their own reactive leniency applications in 2002 and 2003.

Armed with the seized physical documents and the highly detailed, corroborating confessions of the leniency applicants, the European Commission spent several years building an airtight legal case. On September 19, 2007, the Commission delivered a landmark antitrust decision (Case COMP/39.168), officially ruling that the companies had operated a series of illegal cartels in clear, prolonged violation of Article 81 of the EC Treaty (which strictly outlaws restrictive business practices and the abuse of market dominance).

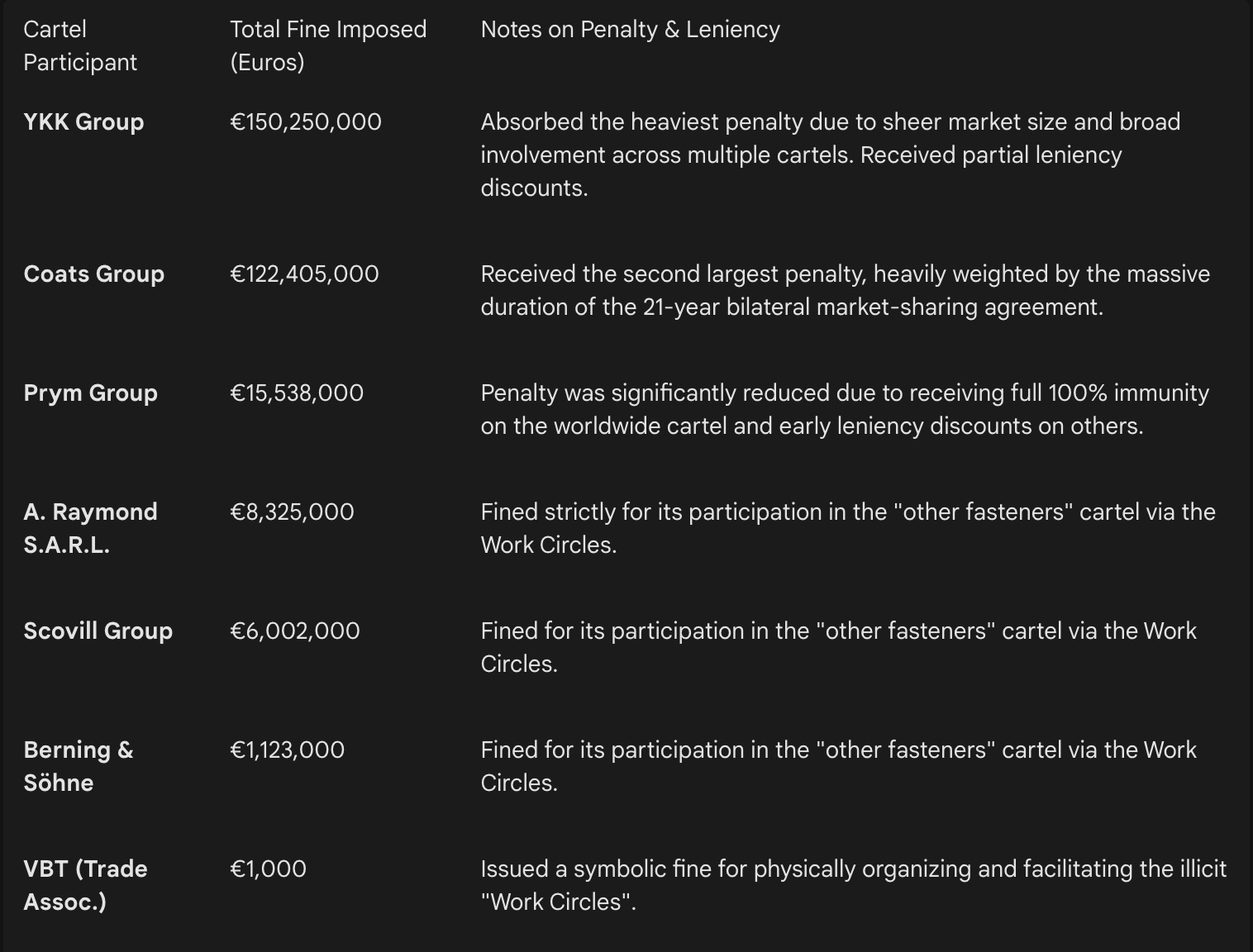

The financial penalties levied by the Commission were severe, calculated mathematically based on the massive size of the affected product markets (clothing, footwear, and industrial goods), the exceptionally long duration of the infringements (ranging from 19 months to 21 years), and the sheer corporate size of the participating firms. The Commission originally announced a staggering total fine of €328.6 million, which was subsequently adjusted to €303.6 million distributed across the various guilty groups.

Beyond the monetary penalties, the Commission's ruling aggressively applied the legal doctrine of “joint and several liability” within complex corporate structures. It determined that parent companies - specifically YKK Corporation headquartered in Japan and Coats Holdings Ltd based in the UK - exercised decisive, operational influence over the commercial behavior of their respective European subsidiaries. Consequently, the parent entities were held financially responsible for the illicit conduct of their regional branches.

This legal mechanism ensures that multinational corporations cannot shield their primary balance sheets by utilizing geographically isolated subsidiaries to conduct illegal cartel behavior: the fines are attached to the ultimate economic entity, ensuring they possess legitimate, deterrent sting.

While the cartel participants largely admitted to the underlying facts of the conspiracy due to their participation in the leniency program, the Commission's specific methodology for calculating the fines sparked legal challenges. YKK initiated a protracted, multi-year appeals process, moving from the European General Court all the way to the European Court of Justice (ECJ). This process culminated in a precedent-setting legal ruling in September 2014 (Case C-408/12 P).

YKK's primary legal challenge did not contest its guilt, but rather pertained to the concept of "successive liabilities" and the strict statutory maximum limits placed on antitrust fines. Under Article 23(2) of EU Regulation 1/2003, an antitrust fine levied against a company cannot exceed a hard cap of 10% of that undertaking's total global turnover in the business year preceding the decision.

The complexity arose from the timeline of corporate acquisitions. During the 1991–2001 “Work Circles” cartel, a German company named Stocko Fasteners participated in the price-fixing conspiracy as an independent company until 1997. In 1997, it was formally acquired by the YKK Group and renamed YKK Stocko Fasteners, at which point it continued to participate in the cartel under YKK's umbrella until the 2001 dawn raids.

The European Commission had originally calculated the fine for YKK Stocko's pre-1997 independent cartel behavior based on the massive 2006 global turnover of its new parent company, the YKK Group, resulting in a €19.25 million penalty for that specific historical period. YKK's legal counsel argued this was fundamentally flawed because the multinational's turnover should not be used to calculate the 10% cap for an infraction committed by a small subsidiary before it was even acquired by the parent company.

The ECJ ultimately agreed with YKK's legal interpretation. The Court ruled that when a subsidiary commits an infraction prior to being acquired by a non-infringing parent company, the 10% fine cap must be calculated solely on the basis of the subsidiary's standalone turnover.

Consequently, the ECJ annulled that specific portion of the Commission's calculation, drastically reducing the specific fine assigned solely to YKK Stocko Fasteners from €19.25 million down to a mere €2.79 million. This legal victory established a vital precedent for M&A due diligence, yet the vast majority of YKK's €150 million penalty remained entirely intact.

Private Enforcement: The U.S. Class Action Fallout

The European Commission’s explosive 2007 announcement served as a primary catalyst for a massive wave of follow-on civil litigation across the Atlantic. While European regulators primarily utilize administrative fines to punish cartels, the United States relies heavily on private antitrust enforcement. Under the Sherman Antitrust Act, direct purchasers who are victimized by a price-fixing conspiracy are legally empowered to sue the cartel members for treble damages, a punitive award equaling three times the actual economic harm suffered by the plaintiff.

Within weeks of the European fines being publicized, 35 major American apparel companies and distributors filed federal class-action antitrust complaints against the cartel members. The plaintiffs alleged that the decades-long global conspiracy directly impacted the US market. They cited specific evidence from the European investigation demonstrating that the cartel explicitly set a specific minimum price for the “rest of the world”, which structurally and artificially inflated the cost of zippers, snaps, and rivets imported into the American apparel market.

The corporate defendants attempted to have the case dismissed before it could reach a jury, arguing that the claims were time-barred under the statute of limitations, given that the cartels ostensibly ended following the 2001 dawn raids. However, in 2011, U.S. District Judge Barclay Surrick firmly refused to dismiss the suit, legally clearing the path for a brutal, highly intrusive discovery phase.

Facing the threat of mandatory treble damages, and the reality that plaintiffs' counsel would utilize the cooperation provisions and documents already secured from the European leniency applicants to prove guilt, the major defendants opted to mitigate their risk and settle.

In early 2014, Judge Surrick granted final judicial approval to a combined class-action settlement totaling $17.55 million. The financial payouts were divided among the primary defendants, mirroring their respective market shares and perceived liabilities: Coats paid $9.85 million, YKK paid $6.6 million, and Prym paid $1.1 million.

Notably absent from the final settlement payout was the American manufacturer Scovill Fasteners. The European regulatory fines proved insurmountable for the company. Scovill filed for bankruptcy protection in 2011 and was subsequently formally dismissed from the class action in the summer of 2013.

Post-Cartel Market Transformation

The dramatic collapse of the cartel, combined with the immense regulatory fines and the distraction of global class-action litigation, catalyzed a profound structural shift in the global fastener oligopoly. While YKK remains the undisputed global market leader today, producing roughly half of the world's zippers, its absolute dominance in the post-cartel era is challenged by a rising Chinese manufacturing powerhouse: SBS Zippers.

Founded in 1984, SBS initially operated strictly in the budget, commoditized tier of the Chinese domestic market, offering cheap components to fast-fashion brands. However, in the vacuum left by the disruption of the legacy European and Japanese cartels, SBS executed a highly aggressive expansion strategy. The company rapidly scaled its production capabilities, pushed its export share to 25%, and heavily invested in in-house research and development teams specifically designed to mimic YKK's vertical integration strategies.

Today, a fierce global duopoly is taking shape. SBS has systematically shifted up-market, securing massive procurement contracts with global athletic and retail giants like Adidas and the French sports retailer Decathlon. SBS achieved this by offering high-quality metal and plastic zippers that rival YKK's legendary durability (guaranteeing performance past 1,000 cycles) but at a significantly lower, highly competitive price point.

In direct response to this existential threat, YKK has been forced to fundamentally adapt its corporate strategy. The Japanese giant is pivoting from its comfortable, high-margin monopoly in the premium and technical segments to compete violently and directly with SBS in the mass-market and budget pricing tiers.

This renewed, intense price competition is the best evidence of the return to a healthy free-market capitalism in the global fastener industry.